What does a smoothed earnings approach mean for the State Pension?

On the back of our successful Pension Promise Campaign, Deputy Seán Canney asked the Minister for Social Protection when the State pension will be increased to 34% of average earnings to meet the Government’s commitment on pensions; and if she will make a statement on the matter. Minister Humphries answered that a smoothed earnings method to calculating a benchmarked/indexed rate of State Pension payments will be introduced as an input to the annual budget process and will be submitted to Government in September each year, commencing this year. (Source: https://www.oireachtas.ie/en/debates/question/2023-06-27/405/#pq_405)

Minister Humphries also mentioned this approach at the Department of Social Protection pre-budget forum at Farmleigh House on 19th July when asked about linking the State Pension to 34% of Average Earnings. The Report of the Commission on Pensions recommends the Smoothed Earnings Approach. This concept is also discussed on Page 41 in the Roadmap for Social Inclusion where it is described as a smoothed earnings system, whereby the rate of pension payment will be linked in the first instance to average wages but, in years where the increase in average wages is less than the rate of increases in prices, it will be linked to the rate of inflation.

While we see this as more secure approach to determining state pension rates, our concern with this response is with the Government’s understanding and definition of average earnings. In the Report of the Commission on Pensions, average earnings exclude over-time, bonus payments etc. It references published CSO earnings statistics – calculating 34% of average earnings (excluding irregular earnings and overtime) and referencing the Harmonised Indices of Consumer Prices (HICP) to calculate a price adjusted rate.

According to Page 26 of the Pensions Commissions’ Working Paper on Benchmarking and Indexation, the use of a base earnings benchmark excluding irregular earnings and overtime is believed to be appropriate for the calculation of a base pension payment. If irregular earnings and overtime were to be included in the benchmark for calculation, then benefits provided to pensioners (e.g., Household Benefits, Fuel Allowance, Christmas Bonus, Free Travel, etc.) would have to be included in the pension payment calculation.

While we understand this rationale, this would not favour a large proportion of pensioners who do not receive any of these types of supplementary supports.

What would be the ramifications if irregular earnings and overtime isn’t included in the average earnings calculations?

By excluding these, the average earnings data would underestimate and under represent the actual income levels of individuals in Ireland. It may fail to capture the full extent of wage gaps and inequities that exist within the population as irregular earnings often vary across different occupations, industries, and demographic groups. This would also limit insights into economic trends and performance as irregular earnings can fluctuate based on economic conditions. To ensure a more comprehensive and accurate assessment of income levels, income inequality, compensation structures, and economic trends, it is important to include irregular earnings and bonuses in average earnings data.

What would be the ramifications for the pensioner?

As the pension rate would be benchmarked to 34% of Average Earnings, the exclusion of irregular earnings and overtime will see a significant drop in the pension rate. Using the latest data from the EHECS (Earnings Hours and Employment Costs Survey) as an example, the difference between the inclusion and exclusion of irregular earnings would be as follows:

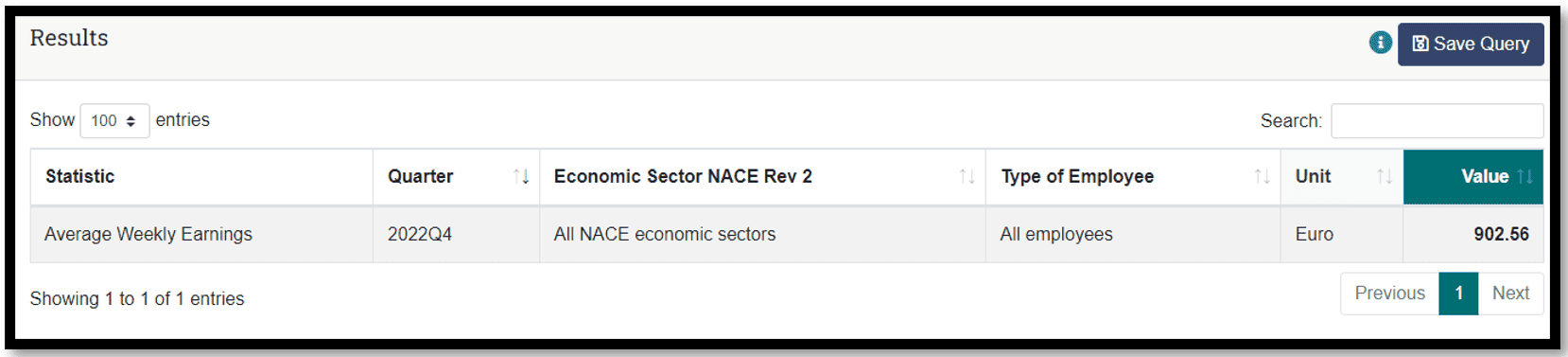

Example 1: Including irregular earnings and overtime

€902.56 is the calculated Average Weekly Earnings from Quarter 4 of 2022. This would result in a weekly pension rate of €306.87

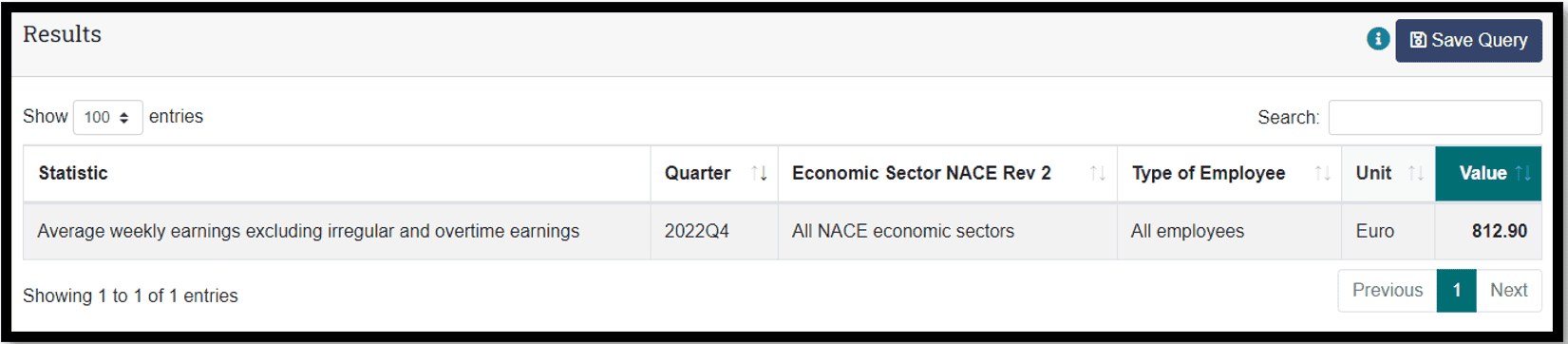

Example 2: Excluding irregular earnings and overtime

€812.90 is the calculated Average Weekly Earnings from Quarter 4 of 2022. This would result in a weekly pension rate of €276.39

This results in a difference of €30 per week, €120 per month and €1440 per year which is a considerable amount for anyone to lose out on, particularly for those with no other source of income.

We ask Government and Minister Humphries to review this method in order to best serve all pensioners by including irregular earnings and overtime in their average earning calculations, ensuring pensioners will end up with more money to help counteract the acknowledged cost-of-living increases.

Posted on 27th July 2023 by Sharon