News

Seniors Trade Show 2023

On Tuesday 17th October, we will be heading to Bundoran in lovely Donegal for the Autumn Seniors Trade Show. We had a wonderful time participating in the Dun Laoghaire-Rathdown Age Well Expo back in June and engaged in enjoyable conversation with the DLR locals. As we received such positive feedback whilst bringing awareness to the issues surrounding older persons, we thought we would head to another part of the country to do the same.

The Seniors Trade Show is taking place in The Great Northern Hotel in Bundoran, Co. Donegal. Each year, the event has been run in different locations around Ireland such as Clare, Mayo and Wexford and the show continues to grow in popularity. The Seniors Trade Show promises to celebrate all that is good about ageing and will focus on areas such as Health, Activity, Financial Security, Travel, Holidays, Lifelong Learning, Social Connections, Sports, Cooking, Fashion, Investments, and Legal Advice. Most importantly, entry is FREE! For more information about the event itself, you can visit www.seniorstradeshow.ie.

WHEN: TUESDAY 17th OCTOBER

WHERE: The Great Northern Hotel, Bundoran, Co. Donegal.

We will be discussing our latest projects and the nature of the work that we do, to support and advocate for our members. We will have some free newsletters and other bits to give away and look forward to speaking to new people about ways in which we can support older persons in Ireland. If you would like to help us out on the day and discuss the work of the ISCP, please contact Niamh at development@seniors.ie

If you would like to attend,

you can register for your free ticket HERE.

***COMPETITION TIME***

If you wish to attend the event with your group, Seniorscard.ie who sponsor the show are holding a competition on Facebook for a FREE BUS TRIP for up to 50 people. Check out their post on Facebook below and be sure to like and share the post for your chance to win.

What does a smoothed earnings approach mean for the State Pension?

On the back of our successful Pension Promise Campaign, Deputy Seán Canney asked the Minister for Social Protection when the State pension will be increased to 34% of average earnings to meet the Government’s commitment on pensions; and if she will make a statement on the matter. Minister Humphries answered that a smoothed earnings method to calculating a benchmarked/indexed rate of State Pension payments will be introduced as an input to the annual budget process and will be submitted to Government in September each year, commencing this year. (Source: https://www.oireachtas.ie/en/debates/question/2023-06-27/405/#pq_405)

Minister Humphries also mentioned this approach at the Department of Social Protection pre-budget forum at Farmleigh House on 19th July when asked about linking the State Pension to 34% of Average Earnings. The Report of the Commission on Pensions recommends the Smoothed Earnings Approach. This concept is also discussed on Page 41 in the Roadmap for Social Inclusion where it is described as a smoothed earnings system, whereby the rate of pension payment will be linked in the first instance to average wages but, in years where the increase in average wages is less than the rate of increases in prices, it will be linked to the rate of inflation.

While we see this as more secure approach to determining state pension rates, our concern with this response is with the Government’s understanding and definition of average earnings. In the Report of the Commission on Pensions, average earnings exclude over-time, bonus payments etc. It references published CSO earnings statistics – calculating 34% of average earnings (excluding irregular earnings and overtime) and referencing the Harmonised Indices of Consumer Prices (HICP) to calculate a price adjusted rate.

According to Page 26 of the Pensions Commissions’ Working Paper on Benchmarking and Indexation, the use of a base earnings benchmark excluding irregular earnings and overtime is believed to be appropriate for the calculation of a base pension payment. If irregular earnings and overtime were to be included in the benchmark for calculation, then benefits provided to pensioners (e.g., Household Benefits, Fuel Allowance, Christmas Bonus, Free Travel, etc.) would have to be included in the pension payment calculation.

While we understand this rationale, this would not favour a large proportion of pensioners who do not receive any of these types of supplementary supports.

What would be the ramifications if irregular earnings and overtime isn’t included in the average earnings calculations?

By excluding these, the average earnings data would underestimate and under represent the actual income levels of individuals in Ireland. It may fail to capture the full extent of wage gaps and inequities that exist within the population as irregular earnings often vary across different occupations, industries, and demographic groups. This would also limit insights into economic trends and performance as irregular earnings can fluctuate based on economic conditions. To ensure a more comprehensive and accurate assessment of income levels, income inequality, compensation structures, and economic trends, it is important to include irregular earnings and bonuses in average earnings data.

What would be the ramifications for the pensioner?

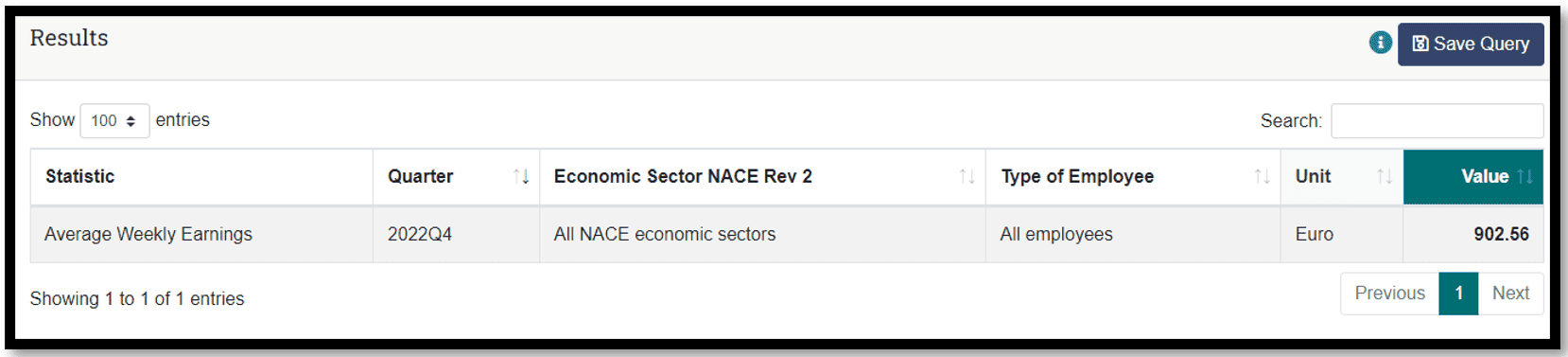

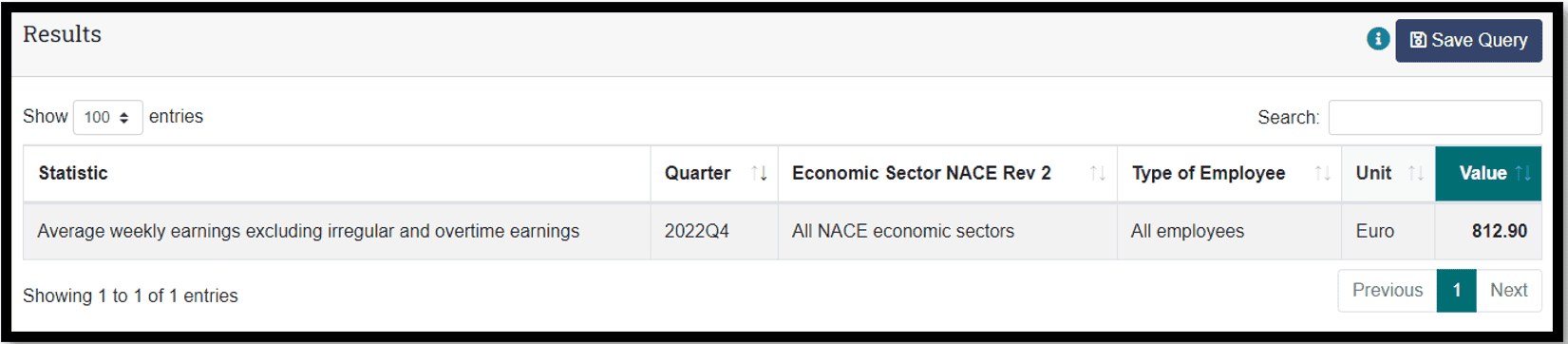

As the pension rate would be benchmarked to 34% of Average Earnings, the exclusion of irregular earnings and overtime will see a significant drop in the pension rate. Using the latest data from the EHECS (Earnings Hours and Employment Costs Survey) as an example, the difference between the inclusion and exclusion of irregular earnings would be as follows:

Example 1: Including irregular earnings and overtime

€902.56 is the calculated Average Weekly Earnings from Quarter 4 of 2022. This would result in a weekly pension rate of €306.87

Example 2: Excluding irregular earnings and overtime

€812.90 is the calculated Average Weekly Earnings from Quarter 4 of 2022. This would result in a weekly pension rate of €276.39

This results in a difference of €30 per week, €120 per month and €1440 per year which is a considerable amount for anyone to lose out on, particularly for those with no other source of income.

We ask Government and Minister Humphries to review this method in order to best serve all pensioners by including irregular earnings and overtime in their average earning calculations, ensuring pensioners will end up with more money to help counteract the acknowledged cost-of-living increases.

Minimum Essential Standard of Surviving

“Due to the cost-of-living crisis, anything less than a €27.50 adjustment in core social welfare rates will be a real term cut. This is the absolute minimum required to prevent individuals and families being pulled deeper into poverty.”

-Vincentian MESL Research Centre Pre-Budget 2024 Submission

The Minimum Essential Standard of Living (MESL) research was transferred from the Vincentian Partnership for Social Justice, to the Vincentian MESL Research Centre at the SVP in July 2022. The MESL research has been ongoing since 2004. The MESL budget standards research has developed to provide an evidence-based benchmark of what is required for a life with dignity for 90% of households in Ireland, and has become an integral part of the policy discourse around income adequacy, poverty and social inclusion.

The MESL expenditure needs dataset is adjusted annually for all household types, to reflect changes in prices. The income calculations used in the Minimum Income Standard (MIS) analysis and the MISc.ie calculator web application are updated each year, incorporating all relevant changes to social welfare and taxation.

The most recent MESL Annual Update Report 2023 has revealed that the cost of the MESL ‘Basket’ has increased by an average of 10.6% nationally predominately driven by the rising cost of food and energy. The MESL basket identifies minimum goods and services that everyone should be able to afford. However, the core MESL basket also assumes that the household is in good health, does not have a disability and also excludes housing, childcare and secondary benefits.

Although the parameters of the MESL Calculations have been reviewed and updated due to the recent hike in the cost of living, they are still based on multiple assumptions which do not accurately reflect the reality for thousands of older persons in Ireland:

- It is assumed that the older person is receiving the highest pension rate of €254 (non-contributory) or €265.30 (contributory)

- The budget allocated to mortgage or rent payments only ranges from €36.60 to €56.70 per week

- The report assumes that the older person is also in receipt of the majority of all bonuses and allowances

- Older persons are also considered to be a full medical card holder

You can view the figures on the MESL 2023 Appendix Tables HERE.

Even with the above assumptions, the MESL research found that the cost of a Minimum Essential Standard of Living for an older single adult living alone has increased significantly since 2022. One-off income supports or additional weekly allowances have not kept pace with the rise in inflation, which demonstrates income inadequacy in 2023.

As we have mentioned in previous articles, the Survey on Income and Living Conditions (SILC) 2022 revealed that persons aged 65 and older had the highest increase in the ‘at risk of poverty’ rate going from 11.9% in 2021 to 19.0% in 2022. As we hear from more and more older persons who are struggling, we imagine that the number of people at risk of poverty has dramatically increased since 2022 and indeed the number of older persons who have since crossed this poverty line.

“The 2023 analysis finds that, for the first time since 2017, neither the Contributory nor Non-Contributory State Pension will provide the basis of an adequate income for an urban older person living alone.”

– Vincentian MESL 2023 Impact Briefing

The Pension Promise Coalition (ISCP, SIPTU, NWCI, Age Action, ARI) have just completed one round of public meetings as part of a campaign where we have been calling on the Government to deliver on its previous commitment to benchmark the state pension at 34% of average earnings. If this system was introduced by next year, the increase would equate to approximately €53 extra per week. The Pension Promise Coalition, Alone Ireland, the European Anti-Poverty Network (EAPN) and multiple other age organisations are calling for the benchmarking of social welfare payments against a level that is adequate to lift people above the poverty line and provide them with at least a minimum standard of living.

Everyone deserves an equal standing in society, an equal opportunity to participate in their community and equal access to an average standard of living. The ISCP continues to try to address this injustice and to ensure that every older person will have security in retirement.

Get the FACTS about the State Pension!

What is the current rate of the state pension?

€265.30 for the contributory state pension and €253 for the non-contributory state pension. Only two-thirds of recipients get the full rate.

What would the rate of the state pension be if it was benchmarked to average earnings?

In 2024, it would be €318/week, €53 more than the top rate contributory state pension at present.

Why should the state pension be 34% of average earnings?

First proposed in 1998, this pledge is developed in The Roadmap for Pensions Reform 2018-2023 and The Roadmap for Social Inclusion 2020-2025, and a technical analysis of the benchmark is conducted as part of the Report of the Commission on Pensions. The Minister for Social Protection has pledged to bring an “input” on benchmarking the state pension into Budget 2024, but this is not the legal certainty that is required.

The 34% benchmark would go some way to reducing the high pension inequality faced by women, carers and people with disabilities.

Will 34% of average earnings eliminate poverty among older people?

No, unfortunately not. But it will provide security because people will know that the pension will increase automatically. Benchmarking would take the politics out of the state pension.

Pension income would need to be 40-50% of average earnings to ensure people are not in poverty in older age. People will need to save for retirement to maintain their living standards, including via auto-enrolment and the important role of occupational pension schemes and personal pension savings.

Why earnings not inflation?

Earnings grow more over time, therefore benchmarking the state pension against earnings will provide older people with a fair share of economic prosperity.

But both is better, which the government has acknowledged in the proposal for ‘smoothed benchmarking’, which will link the state pension to average earnings but give a boost to pension incomes when inflation is higher than earnings growth, after which earnings will have to catch up before the pension would go up again.

Why is legal certainty about benchmarking required?

Without legal certainty, the state pension rate would remain a ‘political football’ in the annual budget, which is why it should be automatic—just like the government is proposing for the annual indexation of income tax bands against inflation.

Weren’t the €12 and one-off payments enough?

No, while welcome, the state pension still lost spending power despite the €12 increase. The one-off payments were not enough to bridge the gap, plus not everyone got them and they only last for one year after which the lost spending power is even more of a problem.

Is it affordable to raise the state pension?

Yes. Raising it by €53/week would cost approximately €1.7 billion/year, at a time when tax and PRSI revenue was €35.4 billion higher in 2023 compared to 2020, which is an increase of over 52%. While revenue linked to multinational corporations may be unsustainable, the state still has strong public finances that can afford to lift older people out of poverty.

In 2021, Irish public spending on old age social protection was 3.5% of GDP or 6.4% of modified GNI, making Ireland the second lowest spender on old age social protection in the EU. The average across the EU was 10.8% of GDP.

Isn’t the Irish state pension rate one of the highest in Europe?

It is sometimes said that the rate of the Irish state pension is higher than in most other EU countries, but this is a deceptive claim.

In Ireland, there is only one tier of state pension providing a basic rate for all, with not everyone getting the full rate. In every other EU country, there is a second tier, top-up state pension based on previous earnings or contributions in addition to the basic rate.

In 2021, in Ireland, pensions from all sources received by people aged 65-74 replace 39% of the earnings from work of people aged 50-59. The EU average was 58% and the highest rates were 81% in Luxembourg and 79% in Spain. Because of the lack of a second tier, Ireland’s pension system had the third lowest income replacement rate in the EU.

Aren’t poverty levels among older people low?

No level of poverty is acceptable, especially for an older person who has no capacity to earn more money to change their circumstances.

The Survey of Income and Living Conditions (SILC) 2022 showed that one in five people aged 65 or older (19%) was at risk of poverty, up from one in ten (9.8%) in 2020.

One in three (33.6%) older people living alone was at risk of poverty, up from one in five (20.5%) in 2020.

Has keeping the state pension age at 66 made raising the state pension unaffordable?

No. Ireland has one of the youngest populations in Europe, and will still have the sixth youngest population by 2070, according to Eurostat projections. This means that we will have the economic capacity to fund a decent state pension and a pension age of 66.

We do have to increase funding for the state pension due to our ageing population, but most of the extra cost is due to the good news that more people are living longer. The Commission on Pensions found that raising the pension age to 68 would only reduce the cost by 16%, with 84% of the extra cost of the state pension due to growing numbers of older people. The Commission calls for PRSI increases to cover the cost of the state pension.

As shown earlier, Ireland’s spending on old age social protection is among the lowest in the EU, so there is a lot of scope to increase that spending without going beyond typically European levels.

Click here to download a PDF version of the Fact Sheet!