News

2025 Pre-Budget Forum with Department of Social Protection

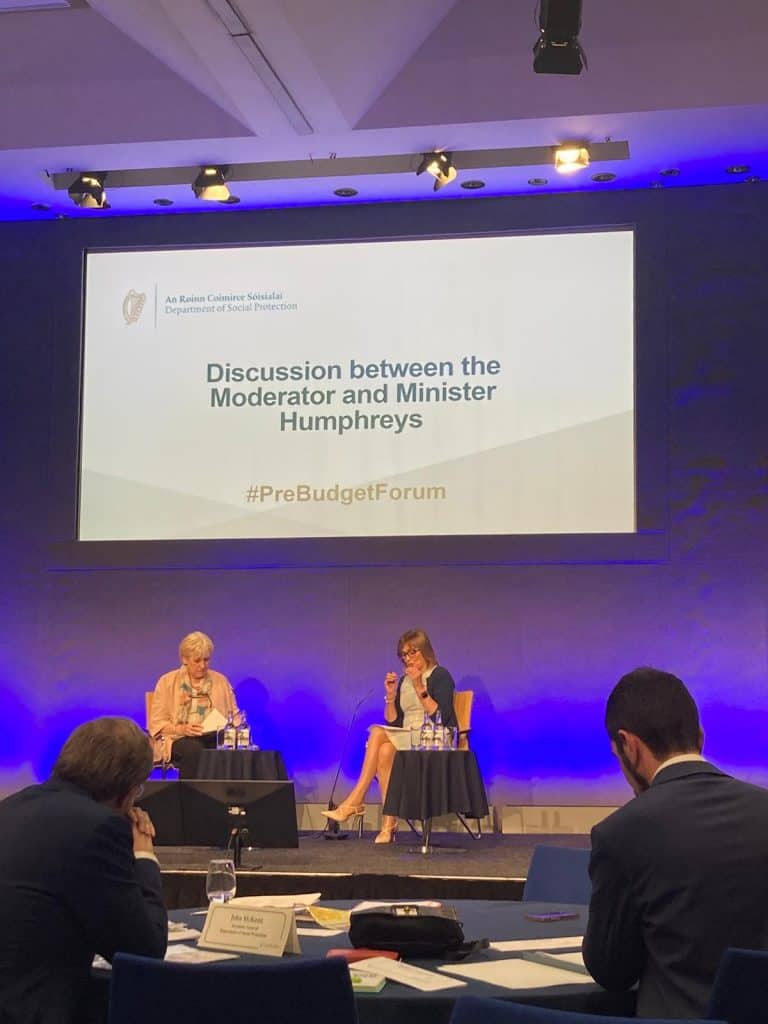

Today marked our annual opportunity to formally speak with Ministers within the Department of Social Protection about the real issues affecting older persons as well as what is most needed in Budget 2025. Welcomed by the wonderful Mary Kennedy, we were treated to an interesting welcome address by Secretary General, John McKeown. He reflected on Ireland’s changing population and cultural landscape while also addressing the well-known fact that our population is ageing. The Secretary General praised the work of the many thousands of people who have immigrated to Ireland and contributed to our society in a positive way. Following this, he expressed the importance of immigrant workers especially within the caring field and suggested that they will be the ones who will be looking after us when “we’re old and decrepit”. We wondered if other colleagues present, working within the age sector, also shared the same worry that this government appears to continue treating our ageing population as a burden.

Secretary General did however reference that this Government “must not react but rather reflect and take action” for the future. He noted that rural depopulation is still in existence which the ISCP have seen, with our older people getting left behind. This point also came up when we broke into our workshop groups to discuss the topic ‘Supporting Retired & Older People’, led by Collum Walsh and Simon Shevlin. This was particularly in reference to pensions, the Living Alone Allowance, Fuel and Cost-of-Living Allowances. We expressed the need for a substantial increase in each of the above as 1 in 10 older persons are living close to the poverty line. We also campaigned for the implementation of benchmarking the state pension and other social supports at 34% of average earnings which was done so in solidarity with all of the Age Sector organisations at the table.

Eligibility criteria, means-testing and income thresholds were also discussed with almost 30% of our members declaring that means-testing social welfare payments had the most negative impact on their financial security. Representatives from each NGO or charity had examples of people being unfairly assessed for much needed supports or being refused one payment because they are not in receipt of another. We expressed the many reports of members who lost their medical card since the €12 pension increase last year expressing the need for more in-depth and transparent cross-departmental communication. Mr. Walsh assured us that each year there is a change to the pension rate, the Department of Health are informed meaning that this error may in fact lie with the Dept. of Health.

Issues with the Qualified Adult eligibility, the Carer’s Pension, Savings in Retirement, Fuel Allowance and the Household Benefits Package were also raised. In a short space of time, we each pleaded our case to Department Officials Colum Walsh, Simon Shevlin and colleagues who were very cooperative and attentive. Mr. Shevlin appeared deeply concerned when we raised the issue of the application and implementation of the Free Travel Scheme, in which one of our members was refused entry to the bus. This sparked debate of other instances where Free Travel Pass Holders have been unfairly discriminated against or left to the side to facilitate pre-booked ticket holders first.

A plethora of statistics, reports and real-life experiences were shared with the Department in the hopes that next year’s budget will be the one that makes a lasting difference for older persons. We are aware that Government cannot possibly satisfy every person’s need but the ISCP feel that older persons have borne the financial brunt of the Irish Economy for far too long. It is well and truly time to restore the purchasing power of our state pension to enable older people to plan for retirement and continue to contribute to the Irish society and economy.

If you would like to read our submission to the Department of Social Protection, you can read the full document here:

2025 Pre-Budget Submission to the Department of Social Protection

Vote Smart, Vote Strong: A Hustings for the near Future

General Elections are fast approaching and it is very possible that these will take place before 2024 is out. So, to help voters prepare for these elections in the best way possible, the ISCP have decided to hold a series of hustings around the country to give older people a chance to question their local candidates before making the all-important decision; Who am I going to vote for?

What are hustings?

Hustings is a panel discussion in the run-up to an election where candidates debate policies and answer questions from the audience. It’s also a great way to secure commitments from candidates, while building relationships with your potential elected representatives. Hustings usually feature candidates from all major parties and are held in the area where the candidates are standing for election. They’re a great way to find out more about where your candidates stand on key issues and to secure commitments which you can later use to hold them accountable, if elected.

How does it work?

The ISCP will host the event, inviting the electoral candidates from the areas we will be visiting. Candidates will sit at the front of the room and are given the opportunity to make an opening statement and then answer questions from the audience with the potential opportunity for candidates to make a closing statement.

Who is it for?

In short, this if for anyone in Ireland who is registered to vote and wants to find out more about each candidate and what they promise to do achieve if elected to Government. We specifically encourage older people to attend these events and ask questions that are most important and relevant to them. It is also imperative to note that candidates should never be guaranteed your vote just because they belong to a specific party or because your family and earlier generations always voted the same way. This is why these Hustings are so beneficial to voters, because the voter gets to directly question each candidate and can decide for themselves if they are worthy of forming part of our government.

Where will we go?

Well, that is up to you. If there is a large hall or event space in your area and more importantly, a large audience of older people who are keen to make an informed decision about our next Government, please get in touch with us.

The ISCP endeavour to give voice to older people in matters such as this and wish to provide as much information to older generations as possible. We want to remind the Government that we are;

Retired Workers – NOT Retired Voters

Collective Network under auspice of ISCP Pensions Meeting on MAY 28th 2024

The Irish Senior Citizens Parliament hosted a meeting to bring together member organisations affected by the lack of a voice regarding their occupational pension. This has resulted in loss of income for many people in an environment of ongoing cost of living increases and hikes in energy costs.

The ISCP formed a collective network some three years ago to address the lack of engagement with pensioners regarding changes to their pension provision. The ISCP supports the progression of the Industrial Relations (Provisions in Respect of Pension Entitlements of Retired Workers) Bill 2021 which is sponsored by Brid Smith. The Bill is before the DAIL and ISCP and the Collective Network of Retired Staff Associations have campaigned heavily to have this progress through all its stages. If passed, the Bill will address the fundamental right of pensioners to be at the table when any decision effecting their pension is being decided. Currently, the Bill is at second stage and is awaiting a report from the Joint Committee.

We thank UNITE for their support in providing the venue on Tuesday 28th of May. We had a full house and were delighted with the turnout from across the country and in particular the engagement of the members on the key issues. The meeting was opened by Pat Mellon, ISCP National Coordinator, who voiced the ongoing commitment of the ISCP to seeing the BILL passed. Eileen Sweeney gave a detailed overview of the work to date on the campaign and Pat welcomed Brid Smith, who took members through the history behind the Bill and its progression to the current stage. She highlighted the disrespect shown to older people by the lack of engagement of the Government on this key issue.

Dr Nat O’Connor from Age Action, whom the ISCP work with on many campaigns, highlighted the reality of income for older people.

“If we look at PAYE income—income that is subject to tax but not including the state pension—of people at the age of 70, the median income—the middle point if you lined people up from lowest to highest income—is €8,136. Half of people at the age of 70 have an income less than that, not including the state pension, but an occupational or private pension income of €8,136 or less. At age 80, it’s €7,700 or less. That’s the middle point. Half of people have more, and half have less.”

In 2022, one in five people aged 65 or older were ‘at risk of poverty’; that is, an income below the poverty line. One in three older people living alone had an income below that line. Dr. O’ Connor went on to explain

“We are sometimes told we have a very generous state pension, but when you look at the European statistics, at income replacement, it tells a different story. Income replacement looks at the income of people in their late 60s and compares this, as a percentage, with the income of people in their 50s. So, to what extent is the pension income replacing work income. You don’t expect it to replace 100%, but the European average is 58%—on average, across Europe, pensions (from all sources) replace 58% of the working income of people in their 50s. In Ireland, it’s 38%—the second lowest in the European Union.”

“Some people like to say that inflation is going down. The inflation rate is a smaller number than it was. But prices are not going down, because it is still a positive number. Inflation is still 2-3%, therefore prices are going up 2-3%. And is your income going up 2-3%? If it’s not, then your spending power is going down. And with 24% inflation, between 2020 when it started, through to the end of next year, then €100 in your hand will buy you what around €80 would have bought you in 2020. So you’ve had the cuts (to state occupational pension funds through the pension levies) and inflation.” The full report from Dr O’Connor is available, so please contact us if you would like more information.

The meeting was addressed by some of the members of the Collective Network on the impact of loss of earnings and having no voice at the table. Paddy Fagan spoke about pension poverty arising from the cuts over the years. John Nugent expressed the urgent need to ensure the lack of engagement by the Government on this issue is addressed.

We thank all who took part in the discussions following the panel inputs and we hope to see you all engaging with your local politicians to create the need to have this Bill passed and to end the inequality and discrimination faced by retired workers and employees.

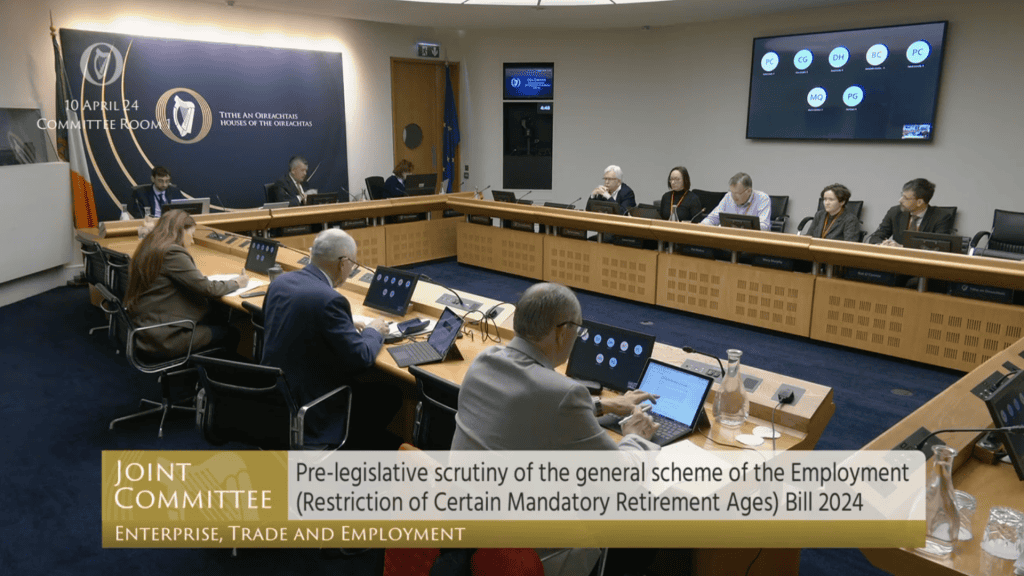

Double Date with Leinster House Debates

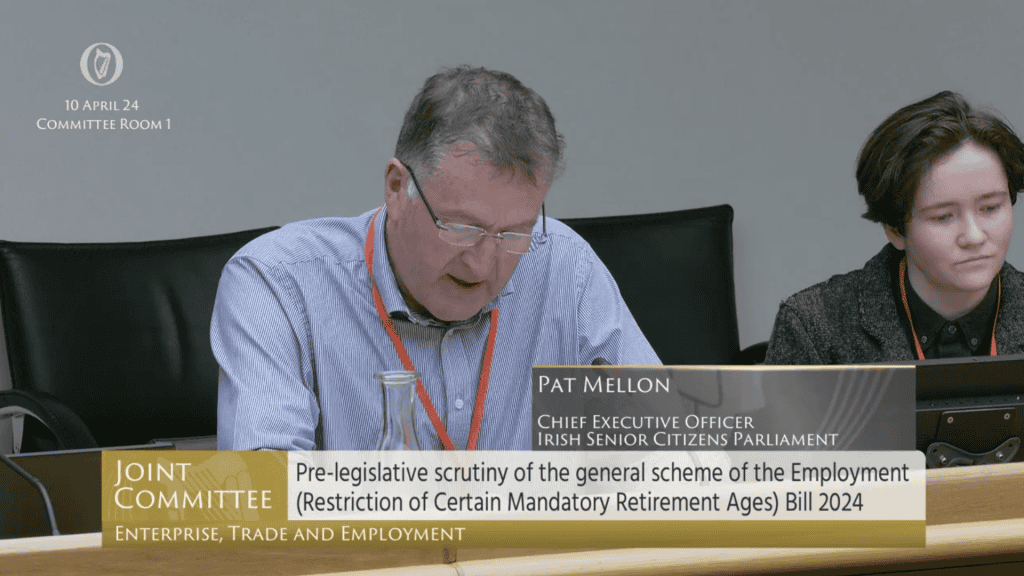

Wednesday the 10th of May was a busy day for the ISCP as we attended two Joint Committee Meetings in Leinster House with the Department of Enterprise, Trade and Employment as well as the Department of Social Protection, Community and Rural Development and the Islands. The first meeting focused on the General Scheme of the Employment (Restriction of Certain Mandatory Retirement Ages) Bill 2024 attended by our National Coordinator Pat Mellon. The aim of the measure is to restrict the enforceability of mandatory clauses in employment contracts where the employee wishes to continue in employment. As recommended by the Pensions Commission, this will deliver a statutory provision which will allow, but in no way compel, an employee to stay in employment until the State pension age.

Pat spoke to the fact that the ISCP strongly believe in the right of older people to choose their retirement age. We believe strongly in the rights of older people to continue to contribute to society in all areas, including choice regarding their working life. In the past few years, we have worked with many retired worker-staff associations whose members have similar experiences and concerns relating directly to their date and age of retirement and the lack of clarity relating to legal age for retirement. Currently, people who had to retire when they reached the age of 65 must seek social welfare benefit payment until they reach the age of 66 and cannot get the State pension or avail of supplementary benefits. He narrated the case of some women in particular who are regarded as an appendage to the assets of their husbands, which is not right.

With regard to the Bill itself, Mary Murphy of Age Action pointed out;

“The Bill does not in fact prevent mandatory retirement at the age of 65 or below; it just changes the requirements the employer must meet. It is not clear that this will even narrow the circumstances in which it can occur, or create any impediment for employers.”

The full debate is available to read HERE.

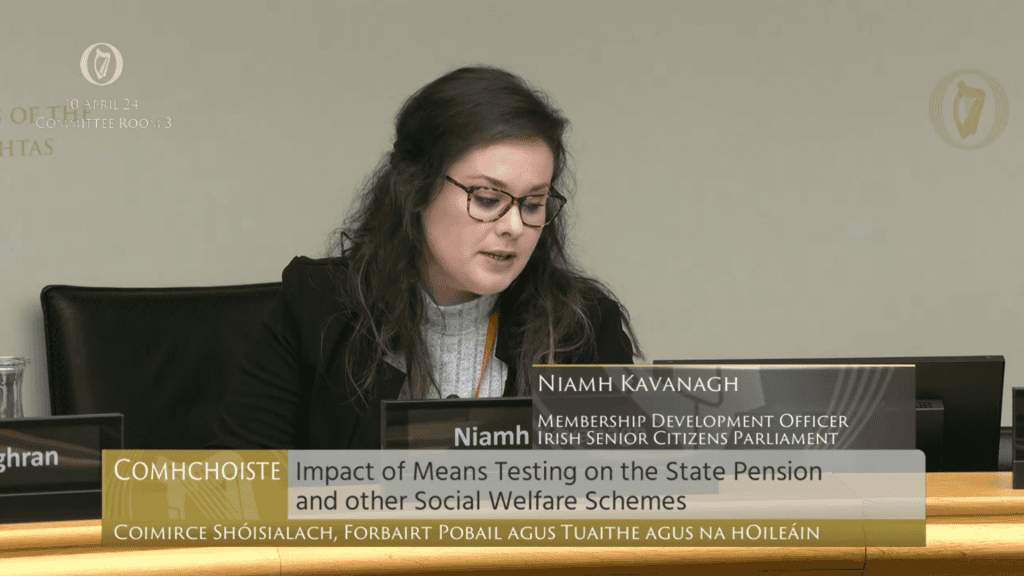

The second Joint Committee meeting discussed the impact of Means Testing on State Pension and other Social Welfare Schemes in which our MDO, Niamh Kavanagh campaigned heavily against;

“What we do not need is more ways of taxing our retirees; rather, we need a system that recognises the needs of those who have reached retirement and need to feel safe, comfortable and valued. Rather than means testing the basic needs of those who have given more than their fair share, a closer look at the pension contributions tax breaks, which very high earners can avail of, may well be a more constructive and equal approach.

There is need for an overhaul of the system to allow for a more effective support to ensure older people and those on other State transfers would have a better standard of living. The ISCP supports a review based on Social Justice Ireland’s call for a universal pension, which would solve many of the problems inherent in the system as it would provide a guaranteed income during old age for all older residents on an individual basis, without regard to anomalies in their social insurance history. It would also provide a secure and certain framework around which individuals can plan for their retirement and, over time, it would distribute income, creating a more egalitarian society.”

Nat O’Connor from Age Action put forward three alternatives to means testing which include universalism, credited social insurance and targeting payments based on other eligibility criteria, not just income or savings, such as, for example, once again giving a medical card to everyone aged 70 and older based on age and not on income.

Sean Moynihan of ALONE commented on the fact that means testing is calculated based on household rather than individual income. Negative impacts resulting from this include cases where older people have been unable to access fuel allowance due to adult children moving back into their parents’ home. Also, something the ISCP have spoken to before, means testing for the non-contributory pension for couples sufficiently impacts individual autonomy and independence in older age, not to mention financial security.

Ireland still spends less money on pensions, which is a function of Ireland’s demographic structure, and relies more heavily on means-tested social assistance rather than social insurance. However, retirement from employment continues to correlate with a decrease in income, resulting in dependence on the State pension for many individuals within Irish society. The growth in wage incomes has outpaced that of State pensions, thereby exacerbating the disparity between the incomes of retirees and employed individuals. The commitment to link the State pension to 34% of the average wage has not been realised, thereby adding further insecurity to pension provision and the gap between rich and poor.

You can read this debate in full HERE.